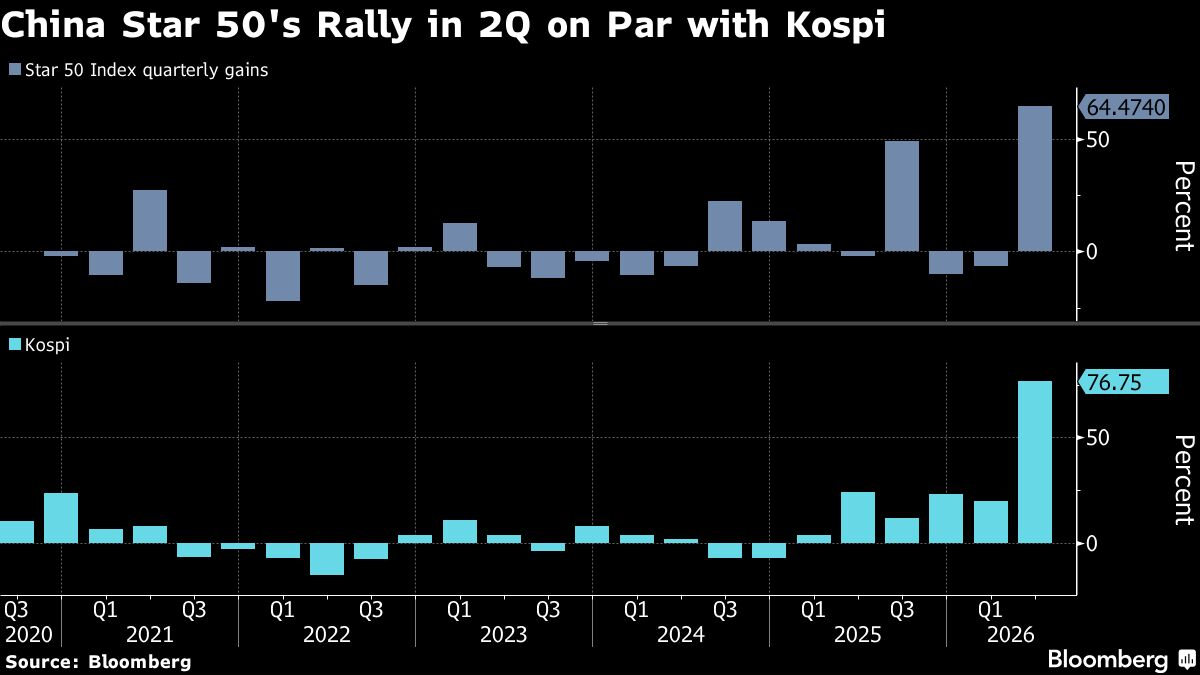

China's Hardware Tech Stocks Are Surging — But the Real Test Is Just Beginning

Chinese hardware technology stocks have delivered one of the most compelling rallies of recent memory, drawing attention from global investors who had long written off the sector amid regulatory crackdowns and geopolitical tensions. Names tied to semiconductors, electronic components, industrial computing, and AI-enabling hardware have climbed sharply, fueled by a combination of government stimulus, surging domestic demand, and optimism around China's push for technological self-reliance. But momentum alone can only carry a stock so far. The next critical test — and the one that will determine whether this rally has lasting legs — is whether companies in this space can deliver the hard earnings numbers to justify their increasingly stretched valuations.

What Drove the Rally in the First Place?

To understand what's at stake for Chinese hardware tech stocks going into earnings season, it helps to understand the forces that sent them higher in the first place. Several structural and cyclical tailwinds converged to ignite investor enthusiasm across the sector.

First and foremost is China's intensifying push toward technological independence. With US export restrictions continuing to limit access to advanced chips and other critical hardware components, Beijing has poured billions into domestic semiconductor production and hardware development. State-backed investment funds, alongside favorable industrial policies, have made the homegrown hardware ecosystem a strategic national priority — and markets have responded accordingly.

Second, the global AI buildout has created an enormous ripple effect. Demand for servers, GPUs, networking equipment, and the full stack of hardware infrastructure needed to power large language models and data centers has been insatiable. Chinese companies positioned to supply any part of that chain — whether domestically or through export — have benefited from this broader wave of capital spending.

Third, improving macroeconomic signals out of China, including government-led consumption incentives and signs of stabilization in the property sector, improved overall risk sentiment toward Chinese equities. This brought foreign institutional money back into the market after a prolonged period of caution.

Valuations Have Run Ahead of Fundamentals

The challenge now is that price-to-earnings multiples across many Chinese hardware tech names have expanded considerably. Stocks that were considered deep-value plays even twelve months ago now trade at premiums that rival their global peers — peers that, in many cases, have far longer track records of consistent profitability.

When valuations move faster than underlying earnings growth, the burden shifts squarely onto the companies themselves. A single disappointing earnings report in a high-expectation environment can unwind months of gains in a matter of days. Conversely, genuine outperformance has the potential to validate the rally and attract a new wave of long-term institutional buyers who have remained on the sidelines waiting for fundamental confirmation.

This is the moment the hardware tech sector now faces. Analysts and investors are scrutinizing upcoming quarterly results with unusual intensity, looking not just at top-line revenue figures but at gross margins, order backlogs, capital expenditure plans, and forward guidance — all the metrics that separate a durable growth story from a sentiment-driven spike.

Key Areas Investors Are Watching

Semiconductor and Chip Manufacturing

Domestic semiconductor producers sit at the epicenter of China's self-sufficiency agenda. Companies in this space have received significant government support, but translating that support into competitive, market-ready products at scale remains an ongoing challenge. Earnings reports will reveal whether production yields are improving, whether design capabilities are advancing, and whether revenue from domestic customers is offsetting reduced access to international markets. Progress in mature-node chip production, where Chinese manufacturers are strongest, will be closely watched.

AI Hardware and Server Infrastructure

The AI infrastructure buildout within China has been a powerful driver of revenue growth for domestic server makers and hardware integrators. Demand from Chinese internet giants, cloud providers, and AI startups for locally produced computing infrastructure has surged. Upcoming earnings should show whether that demand translated into actual recognized revenue and, critically, whether it came with healthy margins or was won through aggressive price competition that compressed profitability.

Electronic Components and Supply Chain Players

Further down the supply chain, makers of passive components, printed circuit boards, connectors, and other hardware building blocks have also caught investor attention. These businesses tend to be cyclical, and their earnings will offer a ground-level view of whether the broader hardware spending cycle is genuinely accelerating or whether inventory restocking has run its course.

The Geopolitical Wildcard

No analysis of Chinese hardware tech stocks is complete without acknowledging the geopolitical dimension. Trade tensions between the United States and China remain a persistent overhang. Further tightening of export controls, restrictions on specific technologies, or escalating tariff pressures could rapidly alter the earnings outlook for companies with significant exposure to international markets or that rely on foreign-sourced inputs. Investors will be listening carefully to management commentary on this front during earnings calls, looking for any signs that companies are insulating themselves through supply chain diversification or accelerated import substitution efforts.

What a Sustainable Rally Actually Requires

Market history suggests that sector rallies driven by narrative and sentiment, without the earnings foundation to support them, tend to be volatile and short-lived. For China's hardware tech stocks to sustain and build upon recent gains, the sector needs to demonstrate a clear and consistent earnings trajectory — one characterized by growing revenues, expanding or at least stable gross margins, and management teams with credible plans for navigating both competitive domestic markets and an uncertain global environment.

The good news is that the underlying demand environment — driven by AI adoption, government procurement, and the broader digitization of the Chinese economy — is real and significant. The question is not whether opportunity exists, but whether individual companies are positioned to capture it profitably and at scale. Earnings season will begin to answer that question, and the results will set the tone for Chinese hardware tech stocks through the remainder of the year and beyond.

- Revenue growth consistency will be the first filter investors apply when assessing whether the rally is fundamentally grounded.

- Margin performance will reveal whether companies are winning business on merit or simply cutting prices to fill order books.

- Forward guidance will signal whether management teams themselves believe the growth story has durability.

- Geopolitical commentary on earnings calls will indicate how exposed individual companies are to ongoing US-China trade friction.

The rally has been impressive. Now the burden of proof shifts from the market to the companies themselves. How they perform over the coming weeks of earnings season will determine whether China's hardware tech moment is a structural shift in global technology investment — or simply the latest chapter in a long history of boom-and-bust cycles in emerging market tech equities.