Wall Street Turns Bullish on the Dollar as Warsh's Fed Era Looms

The US dollar is finishing one of its strongest months in more than a year, and the mood on Wall Street has shifted dramatically in its favor. A growing number of major banks and institutional investors are reversing their previously cautious stances on the greenback, signaling what many are calling a meaningful turning point for the world's reserve currency. At the heart of this renewed enthusiasm lies the prospect of a new Federal Reserve era under Kevin Warsh — a development that markets appear to be pricing in with increasing conviction.

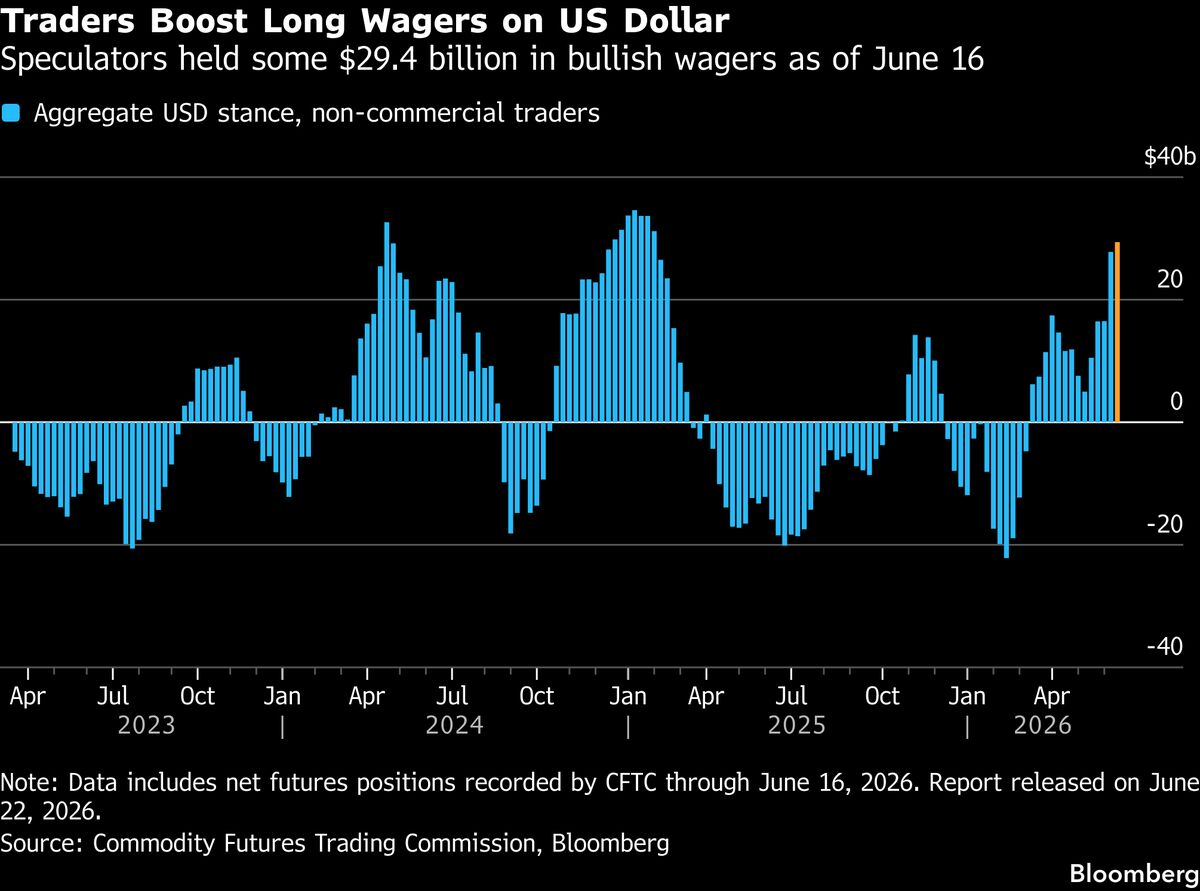

The Dollar's Remarkable Monthly Rebound

After months of pressure stemming from fiscal concerns, shifting rate expectations, and geopolitical uncertainty, the US dollar has staged a noteworthy comeback. The currency is wrapping up one of its best monthly performances in over a year, clawing back losses that had led some analysts to question its long-term dominance as the global reserve standard.

The DXY index, which measures the dollar against a basket of major currencies including the euro, Japanese yen, and British pound, has climbed meaningfully as macro tailwinds aligned for the first time in several quarters. Traders point to a confluence of factors: a resilient US economy, persistent inflation data that has tempered expectations for aggressive Federal Reserve rate cuts, and renewed institutional demand for dollar-denominated assets.

For currency strategists who had been calling for a weaker dollar earlier in the year, this reversal has prompted a swift reassessment. Several high-profile trading desks have updated their models, trimming bearish positions and, in some cases, flipping entirely to net-long dollar exposure.

Why Wall Street Banks Are Changing Their Tune

The turnaround in Wall Street sentiment is not merely a technical reaction to price action — it reflects a deeper reassessment of the fundamental outlook for the US economy and monetary policy. Several major banks have published revised currency forecasts in recent weeks, each pointing to structural reasons why the dollar could maintain or extend its gains.

Key arguments cited by bullish strategists include:

- US economic outperformance: Despite global headwinds, the American economy has continued to grow at a pace that outstrips many of its developed-market peers, keeping demand for dollar assets elevated.

- Sticky inflation dynamics: With inflation proving more persistent than the Federal Reserve initially anticipated, the window for significant rate cuts has narrowed, supporting higher US yields and, by extension, the dollar.

- Safe-haven demand: Ongoing geopolitical volatility — from conflicts in Eastern Europe to tensions in the Asia-Pacific region — continues to funnel capital into the perceived safety of US Treasury bonds and the dollar.

- Capital flow trends: Foreign direct investment and equity inflows into the United States have remained robust, underpinning structural demand for the greenback regardless of short-term rate differentials.

Together, these forces have created a more favorable backdrop for the dollar than existed just a few months ago, and Wall Street appears increasingly willing to position accordingly.

The Warsh Factor: A New Fed That Markets Are Watching Closely

Perhaps the most intriguing element of the current dollar rally is what analysts are calling the "Warsh effect." Kevin Warsh, a former Federal Reserve governor and widely discussed candidate for a future leadership role at the central bank, is seen by many market participants as a hawkish, inflation-focused policymaker. The mere anticipation of a leadership shift at the Fed in his direction appears to be influencing market pricing.

Warsh has historically advocated for a more disciplined approach to monetary policy, with a strong emphasis on price stability and a cautious attitude toward balance sheet expansion. If he were to assume a prominent role at the Federal Reserve, many analysts believe the institution would lean more hawkish than it has under recent leadership — a scenario that would be broadly supportive of the dollar.

Currency markets, which are forward-looking by nature, have begun pricing in this possibility. The result is a preemptive bid for the dollar that compounds the already supportive macroeconomic environment. For traders and investors, this creates a layered thesis: even if the near-term economic data softens somewhat, the prospect of a more hawkish Fed leadership provides a floor under the currency.

What This Means for Global Currency Markets

A stronger dollar has wide-ranging implications beyond the United States. Emerging market economies that carry significant dollar-denominated debt face greater repayment burdens as the greenback appreciates. Commodities priced in dollars — including oil, gold, and agricultural products — typically experience downward pressure when the currency strengthens, affecting everything from energy costs to food prices globally.

For European and Asian exporters, a rising dollar can provide a short-term competitive advantage by making their goods relatively cheaper in US markets. However, the flipside is imported inflation and pressure on central banks abroad to respond with their own policy adjustments.

Currency strategists will be watching closely whether the dollar's momentum can be sustained beyond this month's gains, or whether profit-taking and shifting data will rein in the rally before it becomes a longer-term trend.

Investor Takeaways: Positioning for Dollar Strength

For individual and institutional investors alike, the current environment raises important portfolio considerations. Dollar strength typically benefits US-focused equity investors and holders of dollar-denominated fixed income, while creating headwinds for unhedged international allocations. Those with exposure to emerging market debt or commodities may wish to review their currency hedging strategies in light of the evolving outlook.

As Wall Street continues to recalibrate its dollar views and the prospect of a Warsh-led Fed keeps markets on alert, one thing is increasingly clear: the greenback is back in focus, and the bulls are back in charge — at least for now.