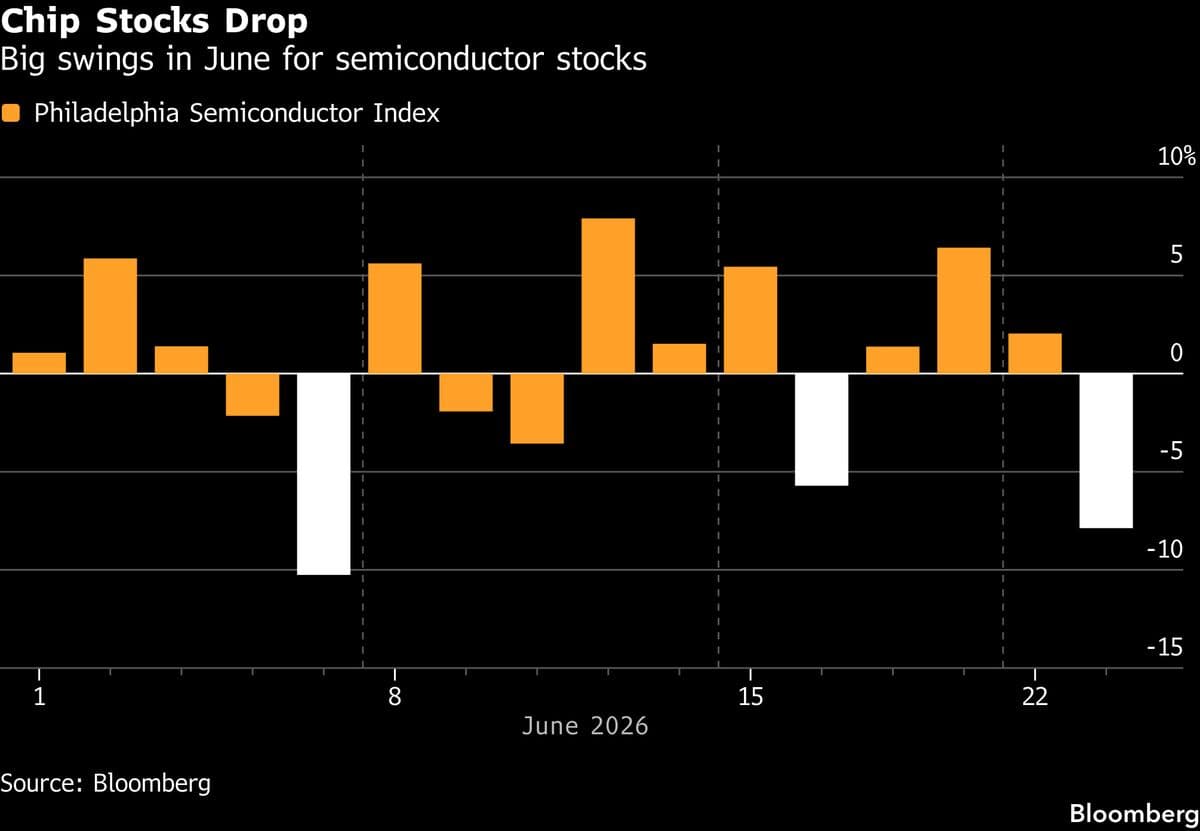

Asia's Stock Rebound Falters as Tech Losses Resume

Asian equity markets struggled to find their footing as a fragile rebound attempt following Tuesday's sweeping global technology-led selloff quickly ran out of steam. What looked like a promising stabilization in early trading gave way to renewed selling pressure across technology-heavy indices, leaving investors on edge and raising deeper questions about the resilience of Asia's markets amid shifting global sentiment.

The episode is a reminder that in today's tightly interconnected financial landscape, a tremor in global technology stocks doesn't simply pass through — it reverberates, often striking twice before the dust fully settles.

What Triggered the Initial Selloff?

The turbulence began with a broad technology-led rout that swept across global markets on Tuesday, dragging down major indices from Wall Street to Tokyo. High-growth technology companies, which had enjoyed an extended period of elevated valuations, came under intense selling pressure as investors reassessed risk exposure in a climate of evolving macroeconomic concerns.

The initial catalyst combined several factors that had been building under the surface for weeks: uncertainty around interest rate trajectories in major economies, concerns about stretched valuations in artificial intelligence-adjacent stocks, and a broader rotation by institutional investors away from growth assets toward more defensive positions.

By the time Asian markets opened on Wednesday, the hope was that the worst had passed and that bargain hunters would step in to support battered technology names. For a brief window, it appeared that hope might be justified.

The Rebound That Wasn't

Early trading on Wednesday saw tentative buying across several Asian technology indices, with investors eyeing oversold conditions as a potential entry point. Markets in key financial hubs, including Tokyo, Seoul, and Hong Kong, initially edged higher as traders positioned for a classic relief bounce following the prior session's losses.

However, the recovery failed to build momentum. Fresh rounds of selling re-entered the market, targeting the same technology and semiconductor-related names that had been hardest hit during Tuesday's rout. The pattern was unmistakable: any attempt to push prices higher was met with resistance from sellers unwilling to hold through continued uncertainty.

This kind of failed rebound is particularly telling from a market structure perspective. When buyers cannot sustain upward momentum even after a sharp decline, it often signals that the underlying sentiment has shifted more meaningfully than a single-day correction might suggest.

Key Markets and Sectors Under Pressure

The technology sector bore the brunt of renewed selling across the region. Chipmakers, hardware manufacturers, and companies closely tied to the global artificial intelligence supply chain all saw continued weakness. Given that many of these companies carry significant weight in regional benchmark indices, their underperformance dragged on broader market performance.

Several dynamics compounded the pressure:

- Semiconductor exposure: Companies across the Asia-Pacific region that supply components to global technology giants saw their shares pulled lower as demand outlook concerns resurfaced.

- Currency sensitivity: A stronger US dollar added an additional headwind for some regional markets, complicating the earnings picture for export-oriented technology firms.

- Global fund flows: Institutional investors rebalancing portfolios away from technology growth stocks contributed to sustained selling pressure that individual retail buying could not offset.

- Sentiment contagion: Negative headlines from US technology markets continued to weigh on investor psychology in Asia, making it difficult for regional markets to decouple from the global narrative.

Investor Sentiment and the Broader Market Narrative

The failure of Wednesday's rebound attempt reflects something deeper than a single day of bad news. It speaks to a more cautious investor mindset that has been gradually taking hold across global markets in 2025. After years of technology stocks leading equity markets to record highs, participants are increasingly asking whether valuations fully account for the risks ahead.

Concerns about the pace of monetary policy normalization in the United States, geopolitical friction affecting global supply chains, and the high expectations baked into artificial intelligence-themed investments have all contributed to a more volatile environment for technology equities specifically.

In Asia, these global pressures are amplified by the region's heavy economic and market exposure to the technology sector. Countries like South Korea, Taiwan, and Japan host some of the world's most critical technology manufacturers, meaning that shifts in global tech sentiment translate quickly and meaningfully into domestic market performance.

What Investors Should Watch Going Forward

For market participants navigating this environment, several factors will be critical to monitor in the sessions and weeks ahead.

First, the performance of US technology stocks will continue to set the tone for Asian markets. Any sustained recovery on Wall Street would provide a meaningful tailwind for regional indices. Conversely, further weakness in US tech names would likely extend the pressure across Asia-Pacific markets.

Second, macroeconomic data releases — particularly those related to inflation and employment in major economies — will shape expectations around central bank policy and, by extension, risk appetite across asset classes. Technology stocks, as long-duration assets, are particularly sensitive to interest rate expectations.

Third, corporate earnings guidance from major technology companies will be closely scrutinized. In an environment where valuations are under question, forward-looking commentary from industry leaders carries outsized importance for investor confidence.

Conclusion: Volatility as the New Norm

Asia's failure to sustain a post-selloff rebound is a clear signal that the technology sector's turbulence is not simply a one-day event. Investors should prepare for an extended period of elevated volatility, particularly in technology-heavy markets across the Asia-Pacific region. Disciplined risk management, diversification, and a close eye on global macro developments will be essential tools for navigating what promises to be a challenging market environment in the months ahead.

As always, markets ultimately price in available information over time — but in the short term, sentiment and momentum can drive meaningful dislocations that patient, well-informed investors are best positioned to weather.