China Moves to Unify Its Yuan Markets in a Bold Currency Play

China is quietly but deliberately reshaping the way its currency functions on the world stage. In its latest policy adjustment, Beijing is bringing its domestic yuan market — known as the CNY — closer in line with its offshore counterpart, the CNH. While this may sound like a technical tweak, the implications are far-reaching. This convergence represents one of the most meaningful steps yet in China's decades-long ambition to transform the renminbi into a true global reserve currency capable of rivaling the U.S. dollar.

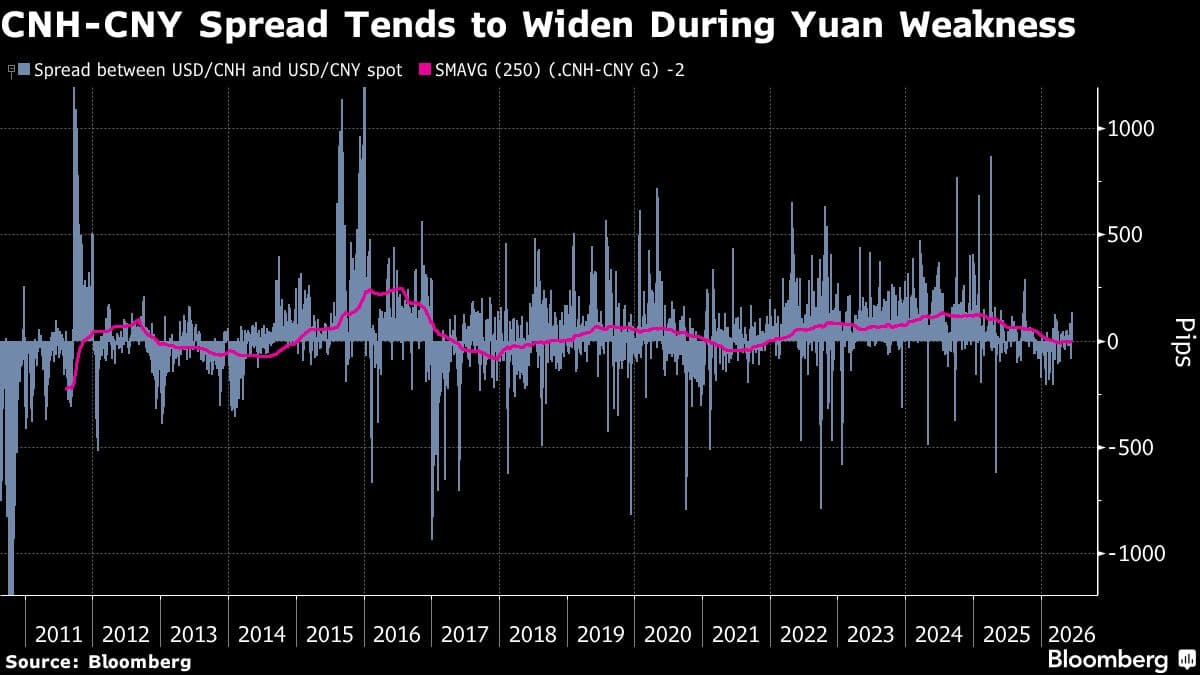

For years, China's dual yuan system has been both a feature and a friction point. The onshore yuan, tightly controlled by the People's Bank of China, operates within a managed exchange rate band on the mainland. The offshore yuan, traded freely in financial hubs like Hong Kong, Singapore, and London, tends to reflect market sentiment more openly and often diverges from its onshore cousin. By narrowing that gap, China is signaling a new level of confidence in its currency — and a new ambition for where it wants the renminbi to go.

Understanding the Dual Yuan System

To appreciate the significance of this development, it helps to understand why China has maintained two separate yuan markets in the first place. When China began cautiously opening its financial system in the early 2000s, policymakers wanted to allow global use of the renminbi without fully surrendering control over domestic monetary conditions. The offshore market was the solution: a semi-separate ecosystem where foreign investors and businesses could trade yuan, settle transactions, and hold renminbi-denominated assets without directly influencing the tightly managed mainland market.

This arrangement gave China the best of both worlds for a time. It promoted international use of the renminbi while insulating the domestic economy from volatile capital flows. But it also created persistent inefficiencies. Businesses operating across both markets had to navigate two different exchange rates, two different pools of liquidity, and two sets of regulatory expectations. The spread between the CNY and CNH rates has at times been wide enough to create significant arbitrage opportunities — and headaches for multinational corporations trying to manage currency risk.

What the New Policy Adjustment Means

China's latest move seeks to reduce that friction. By bringing the two markets closer together — whether through expanded quotas, harmonized pricing mechanisms, or streamlined cross-border capital flow rules — Beijing is effectively telling the world that it trusts the renminbi to operate in a more unified, transparent environment. This is not full capital account liberalization, but it is a meaningful step in that direction.

The practical effects could be significant for businesses and investors. A narrower gap between onshore and offshore rates means more predictable currency exposure, lower hedging costs, and greater confidence that the price of yuan in Hong Kong reflects something close to its value in Shanghai. For multinationals that invoice trade in renminbi, this kind of consistency lowers transaction costs and reduces the administrative burden of navigating a fragmented currency system.

For global investors, a more unified yuan market is also a more liquid and trustworthy one. Greater convergence signals that Chinese authorities are comfortable allowing market forces to play a larger role in determining the renminbi's value — a key prerequisite for any currency aspiring to reserve status.

The Bigger Picture: Renminbi Internationalization

This policy shift does not exist in isolation. It is the latest chapter in a long-running effort by Beijing to expand the renminbi's role in global trade and finance. That effort has included the launch of the Cross-Border Interbank Payment System (CIPS), a yuan-denominated oil futures contract in Shanghai, the inclusion of the renminbi in the International Monetary Fund's Special Drawing Rights basket, and a growing network of bilateral currency swap agreements with central banks around the world.

Despite these efforts, the renminbi still accounts for a relatively small share of global foreign exchange reserves and international payments compared with the dollar, euro, and even the pound and yen. Structural barriers — including concerns about capital controls, rule of law, and the depth of China's financial markets — have slowed adoption. But geopolitical shifts, particularly Western sanctions against Russia and growing interest among Global South nations in reducing dollar dependence, have created new momentum for renminbi alternatives.

Challenges That Still Lie Ahead

Bringing the onshore and offshore yuan closer together is a positive step, but it is not a panacea. Investors and trading partners will be watching carefully to see whether China follows through with the deeper structural reforms that genuine currency internationalization requires.

- Capital account openness: Full convertibility remains a long-term goal, not a near-term reality. Restrictions on capital flows continue to limit foreign participation in Chinese financial markets.

- Regulatory transparency: Global investors want predictable, rules-based financial regulation. China's regulatory environment, while improving, still carries significant uncertainty.

- Market depth: A truly global currency needs deep, liquid bond and equity markets where foreign institutions can park large sums without moving prices significantly.

- Geopolitical risk: Tensions between China and Western economies add a layer of risk that makes some central banks and institutions reluctant to increase renminbi exposure.

A Currency Evolving in Real Time

What makes this moment notable is the pace of change. China's currency policy has historically moved slowly and cautiously, with each liberalization measure carefully calibrated and tested before the next one is introduced. The decision to link the offshore and onshore yuan more closely suggests that Beijing believes conditions are now right to move faster — and that the renminbi is ready for a larger role on the world stage.

For businesses trading with China, financial institutions active in Asian markets, and central banks diversifying their reserve portfolios, this development deserves close attention. The gap between the yuan China uses at home and the yuan the world uses abroad is narrowing. And as it does, the renminbi's claim to genuine global currency status grows steadily stronger.